Silicon Valley Bank: Who Are They, What Happened, and What's Next

Silicon Valley Bank: Who Are They, What Happened, and What's Next

What happens when a bank run hits the tech world

Welcome to the second round of Insufficient Data! This past week we’ve seen a wild ride of panic in the banking market, VC alarm bells, and regulatory action. So what does it all mean? I’ll try to break down who the players are, what happened, and what’s next. There’s a lot of context needed both on the banking and tech sides, so it’s a high word count kind of week.

Who is Silicon Valley Bank?

Since last Thursday, Silicon Valley Bank has been the primary concern of everyone in tech and banking. They’ve been around for almost 40 years and are the go-to bank for startups in Silicon Valley. Because of this, they’ve become a relatively large regional bank - by the end of 2022, they were the 16th largest bank in the country with $209B in assets. 44% of venture-backed tech or healthcare companies that IPOed in 2022 had an account with SVC. If you’ve worked for a startup in Silicon Valley in the last decade, it’s highly likely that your company used SVB at some point.

There are several reasons why SVB was popular among startups. First, it was what VCs recommended to their portfolio companies. They had their own investment arm that invested directly in startups and placed money in other VC funds, so this led to a warm relationship with the VC ecosystem. Additionally, they offered fairly uncommon benefits to startup founders (and, to some extent, startup employees). They provided special loan deals to founders, a streamlined process for opening an account without a social security number (a key feature given a large number of foreign-born startup founders), and lending against pre-IPO shares. And they had several complementary business services like rolling lines of credit that helped startups with rolling user acquisition costs that would be recouped later.

These features made them a great option on paper for many startups. However, that also gave them a unique profile of depositors. When many of your depositors are in a dense network (startups), their deposit and withdrawal behavior can be highly correlated. So when a few companies start taking out their deposits, they tell their founder WhatsApp group what they did or make a Twitter post inciting more withdrawals. That was the case with SVB. And that correlation is one reason why other regional banks likely didn’t follow suit to court such a narrow niche of startup customers.

Some background on bank runs

A standard mental model for how banks function is that they take the deposits of people and businesses who want to store money, and they keep some fraction of that money at the bank in case someone wants to make a withdrawal. They use the rest of the money to make loans or invest in other assets to earn interest. This is commonly referred to as fractional reserve banking, and it’s pretty much how banks work worldwide. Of course, a small group of folks don’t like fractional reserve banking.

While there are some quibbles among economists that fractional reserve banking might amplify economic instability, it’s a primary reason we can quickly get loans at our local bank, and small businesses have easier access to capital. Capital availability is essential when we think about the velocity of money in the macroeconomy, so I don’t see this system being torn down anytime soon. Without fractional reserve banking, we would need a capital substitute to provide easy loans to small businesses and households, and additional capital to provide market liquidity for certain types of securities.

So what is a bank run? A bank run happens when many customers ask for their deposits back all at once. Since the bank only has a fraction of the deposits available at any one time, it faces a liquidity problem. As word gets out that the bank is illiquid, other people try to pull out their deposits, and by that time, it’s too late. The bank doesn’t have the money, so they may try to sell assets that haven’t matured for a discount, but then losses start piling up, and they go into a death spiral. It’s (approximately) what happened in It’s a Wonderful Life.

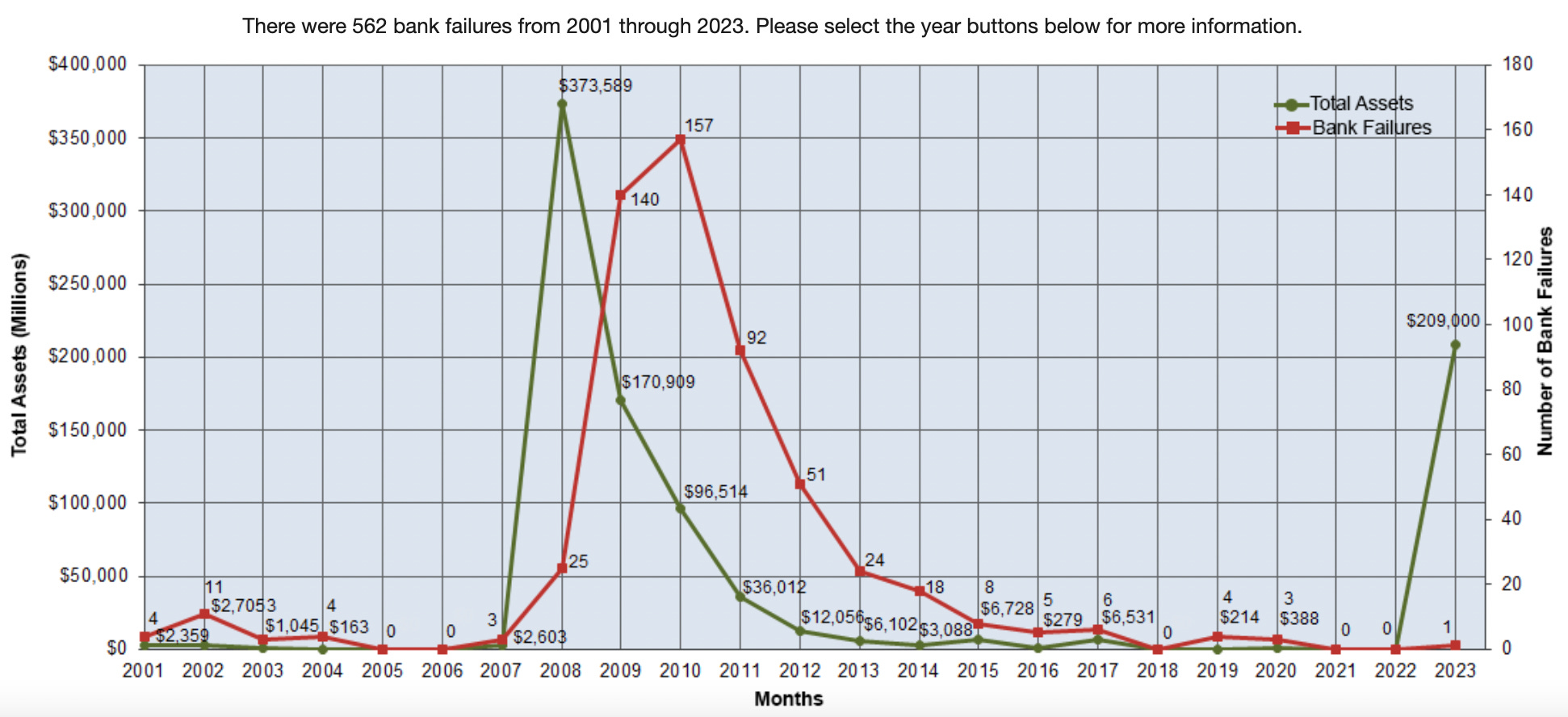

However, bank failures are a relatively common phenomenon. Since 2001 there have been 563 bank failures where the FDIC has intervened.

The FDIC was created in 1933 by President Franklin Roosevelt to build confidence in the banking system after the Great Depression. They provided insurance to guarantee deposits up to a limit. Insurance premiums paid by member banks fund the program, and no taxpayer money is needed to maintain the insurance. Since the start of the program, all insured funds have been recovered. Like any good insurer, they also have a certain amount of supervisory responsibility over the banks to ensure they are responsible with their deposits and not doing any crime. This supervisory responsibility is granted by the US government and outlined in several congressional bills and executive acts.

What happened to the banks?

I mentioned before the basic fractional reserve banking model, where a bank takes money from deposits to make investments. In this regard, SVB has a fairly unique liability and asset profile. Because they are the banker-of-choice to many startups, their accounts tend to be large (over $4m balance on average). Since the FDIC only insures up to $250,000 per account, a large percentage of their deposits are uninsured by the FDIC. They have the second largest percentage of uninsured deposits at more than 93% (BNY Mellon has a larger percentage, but they serve a different clientele). If a bank run happens, the risk of losing your money is much higher since the FDIC doesn’t cover you. Additionally, 2022 saw a retreat for venture funding which meant many startups were already drawing down their deposits rather than adding new venture capital funding to their accounts.

Their assets are where investors started seeing the most worrying trends. Banks tend to hold assets of various maturities to hedge risk. They may have some portion in short-term bills that are very liquid and not particularly sensitive to interest rates (but more sensitive to short-term market volatility). They will also hold some longer-term securities with maturities of months or years that carry a lot of interest rate risk but are relatively insensitive to short-term volatility. The overall profile of what assets a bank holds and the maturity date on those assets determines a risk-weighted measure of their assets.

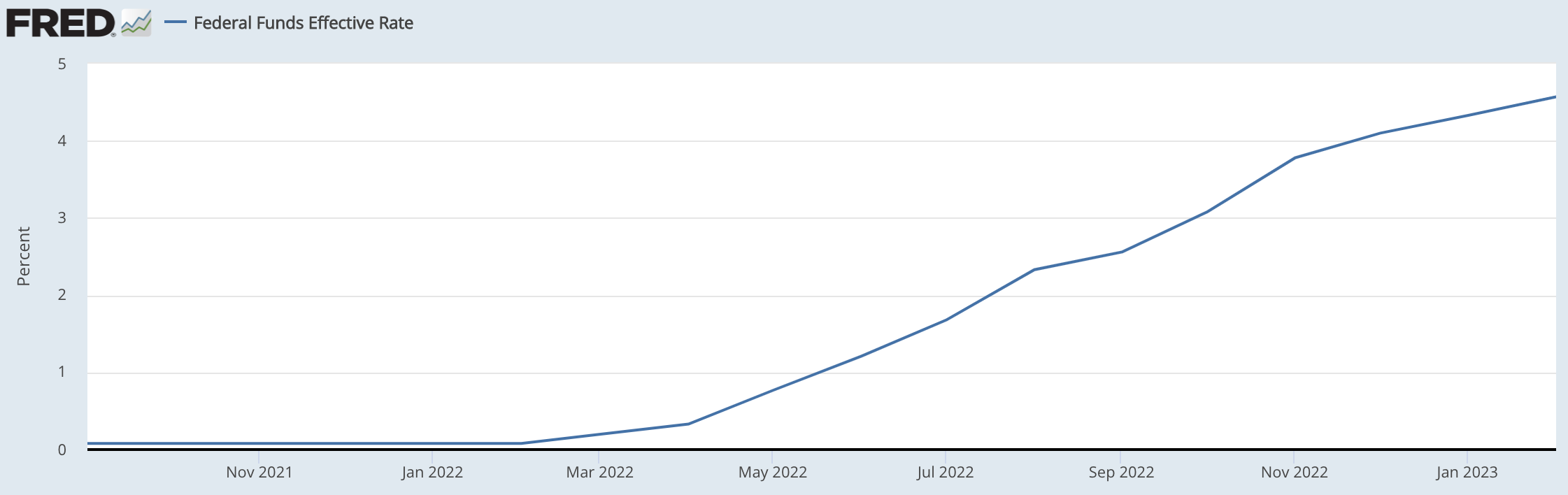

Given that startup deposits are interest-rate sensitive because VCs will tend to deploy more capital when interest rates are low, and capital is easy to come by, you might think that it would make sense to hold assets that are less sensitive to interest rates, so you don’t have correlated risk across your assets and liabilities. Unfortunately, that’s not what SVB did. The federal funds rate has started to climb in the last six months.

SBV’s holdings comprised many long-term treasury bonds and mortgage-backed securities (MBS). Over 55% of the securities that SVB owned were long-term. With interest rates rising, this meant that their asset portfolio was losing value. Because of the high risk correlation between their assets and liabilities, this meant that they're likely to have their deposits called at the same time their assets are performing poorly. When customers started asking for their deposits, they had to realize those losses by selling the bonds at their current market price. They reported these losses immediately, which the market took as a negative signal. This caused more panic among account holders, and at that point, the bank run was self-fulfilling.

Many VCs cited Byrne Hobart’s newsletter as the initial alarm regarding SVB’s balance sheet. He correctly spotted the risk in SVB’s balance sheet with regard to their interest rate risk and long-maturity assets.

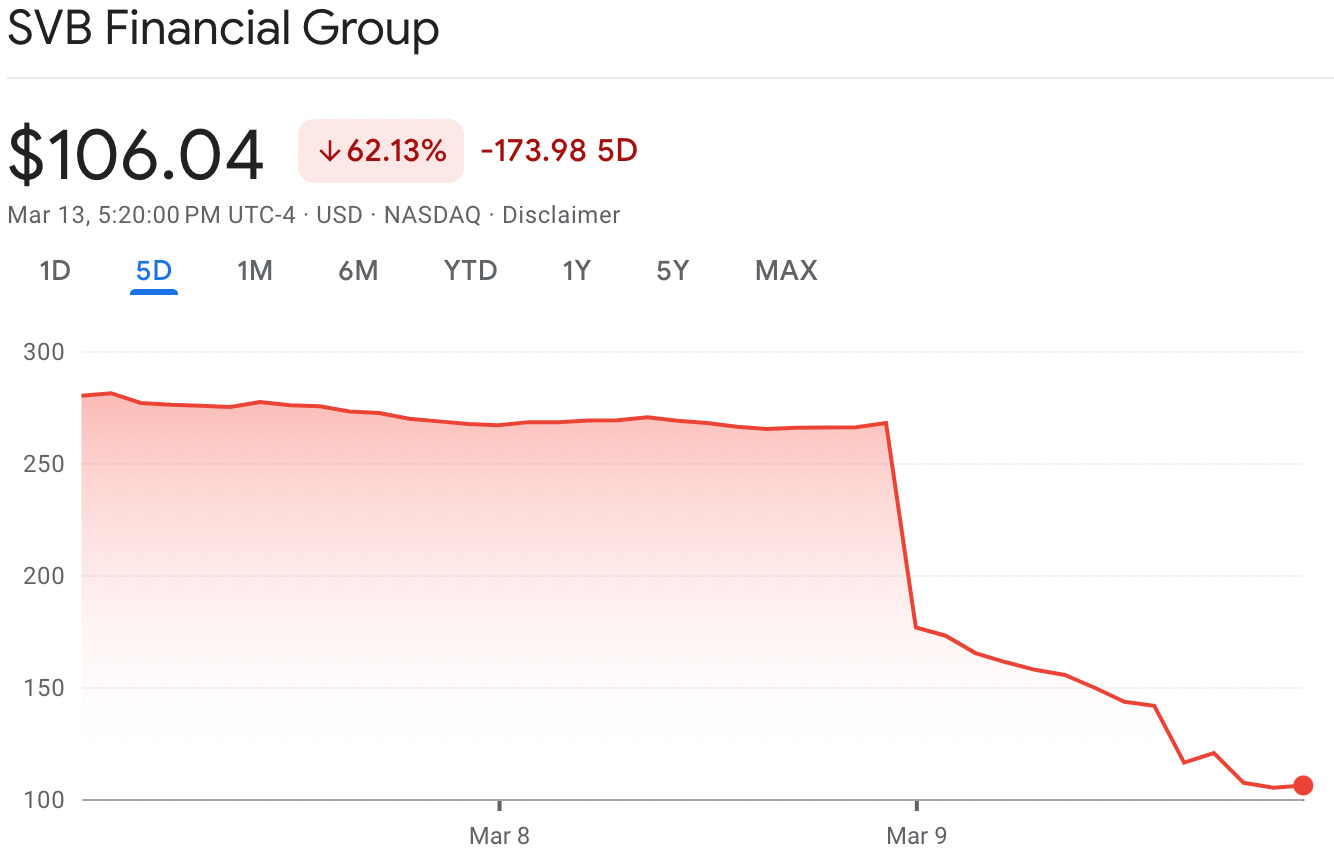

Last Wednesday and Thursday, there were already a lot of whispers in the tech community that SVB was going under, and several VCs started telling their portfolio companies to pull their deposits out. On Friday, March 10th, SVB was closed by the FDIC and put into receivership. All the bank’s officers were let go. They received requests for $42B in deposits on Thursday. It was the second-largest bank to fail in the FDIC’s history. The FDIC’s receivership process means the bank is closed and put into an FDIC holding company, and its assets are sold to pay back those with deposits (and other creditors thereafter).

Reports started coming in of startups with significant liquidity issues if they couldn’t access their SVB account. Many smaller startups had all of their money at SVB, and even larger startups had a considerable portion. With March 15th being a payroll date for many companies, this meant that they might not be able to pay employees. Some VCs started offering to cover payroll until a better solution was figured out, and others took to Twitter to ask for a government bailout.

On Sunday, Signature Bank was added to the list as the second bank to fail this year. Signature Bank was a somewhat different case in terms of their balance sheet, but they suffered a bank run of $10B in deposit requests on Friday as news of SVB’s distress spread. They were a crypto-friendly bank that some say was punished by regulators for tying the crypto system to the traditional financial markets. Some bank managers said they thought they could survive the run on deposits as late as Sunday morning, but soon thereafter, the FDIC announced their receivership.

In the aftermath over the weekend, there was a lot of discussion on Twitter about what regulators should do and what startups should expect. Much of it was panic, but also a lot of misunderstanding about how banking regulation works and how the FDIC and Treasury typically approach bank failures.

Of course, some commentaries were political, blaming the opposite side for the bank failure or the response (or lack thereof).

So what’s the status?

On Sunday afternoon, the FDIC, Fed Chair, and Secretary of the Treasury announced that 100% of deposits would be backed by the Deposit Insurance Fund (DIF) and available Monday morning. They did not find a buyer for the whole bank but are selling assets separately. Typically a single buyer will guarantee a portion or all deposits upon purchase (such as when JP Morgan bought Washington Mutual in the largest bank failure in US history in 2008), but when that doesn’t happen, the FDIC will auction them for the best price they can get. We’ve also seen the SVB UK division sold to HSBC to rescue their operations in the UK.

Signature Bank was also offered the same DIF backstop as SVB on Sunday, guaranteeing 100% of deposits to calm the market further. In both cases, any losses will be paid by the DIF, not taxpayers. By traditional definitions, this is a natural insurance function, but some still call it a government bailout even though no taxpayer money will be used.

What to expect this week

Bank stocks tumbled when markets opened this morning, showing that there’s still a lot of negative sentiment. First Republic Bank and PacWest Bancorp are two regional banks that experts are watching for further bank runs after their stocks dropped 72% and 63%, respectively.

On Tuesday the consumer price index (CPI) will be released and on Wednesday, the producer price index (PPI) numbers will be released, which are the last major statistical releases before next week’s Federal Reserve FOMC meeting. This will give us an indicator of where inflation is heading. Goldman Sachs’ economists predict no movement in the federal funds rate after last week’s bank runs.

Over the coming days and weeks, we’ll also start to see what assets are sold from SVB and on what terms. That will determine how much money needs to be taken from the Deposit Insurance Fund. Based on the FDIC’s announcement, any funds not recovered from asset sales will be taken from the fund and paid by member banks. Like personal insurance, banks have to pay an insurance premium for FDIC insurance, so I would also expect some discussion of changes in the premiums banks currently pay for deposit insurance.

And finally, as expected, SVB is being sued by shareholders for fraud (as Matt Levine always says, everything is securities fraud). So expect to see news coming out about what bank officers knew about the potential for risk and weakness leading up to the bank run.

Other questions

Even after the FDIC announcement on Sunday, several questions remain regarding banking regulation, the tech ecosystem, and labor markets.

How did this affect the VC ecosystem?

Many VCs were touting their predictions and influence after the FDIC’s announcement.

It was not a great look for VCs as many of them yelled (in all caps!) into the ether that global catastrophe was coming or that they needed a bailout. I wouldn’t go so far as to blame VCs for the bank run, but telling companies to pull money and writing panicked tweets surely didn’t help. There were multiple instances of VCs and founders calling the bank run a Prisoner’s Dilemma and saying that it was rational for them to be having everyone pull out. Unfortunately, they didn’t understand the rules of the game, and I think Matt Darling said it best.

I’m sure it will lead to some discussion with limited partners about how the portfolio chooses banks. Some founders are already mentioning they expect future funding to be tied to using a big bank for their accounts. Some VCs silently showed up for their portfolio and offered money for payroll and support going forward. Still, I suspect most people will primarily remember the loud Twitter declarations.

How will this change startup banking?

There are a few lines of thought concerning startup banking. One is that all startups will move to the largest four or five banks that are essentially “too big to fail.” The government will back up these banks due to their systematic importance in the financial industry. In the interim, this would not be surprising while the policy settles.

Another line of thought is that middleware will become king. New financial startups will pop up, which makes opening many accounts easy and provide a single interface for startups. Right now, having a startup with 20 bank accounts to hold your $5m balance so that it’s all FDIC-insured would be a hassle and not easy to integrate. The software could obfuscate that hassle for a small fee. This is possible but unlikely for now due to some apparent policy changes, which I outline below.

How will banking regulation and policy change?

If you had asked me over the weekend what FDIC policy might change due to this, the two areas I would cite are increased coverage for larger account sizes and requirements for more reporting and stress testing of smaller banks, like what was originally envisioned in the Dodd-Frank Act. I still think the second is true, but Sunday’s announcement made me question the first.

Along with the deposit announcement for SVB, the Fed announced the terms of a new Bank Term Funding Program (BTFP) that would be used to lend to banks. The critical part of the announcement was that loans would be issued against bank assets and valued at par. Traditionally, assets are valued at current market value, so if you have long-term assets that dropped in value because of an interest rate hike, you would have to accept a lower value. Now banks can value them at their full maturity value, leading to higher loan thresholds. This should mean that banks can weather more turbulence without needing to trigger insurance coverage. It also means the Fed is taking on more risk, but then again, as a lender of last resort, that has always been its role to a lesser extent. They still might pair this with higher account limits for FDIC deposit insurance (assumedly with higher premiums as well), but I don’t think that’s as important a topic now as it was before the BTFP.

The area that remains an important policy consideration is reconsidering the legislation passed in 2017 to make smaller banks immune to some of the reporting requirements outlined initially in Dodd-Frank. SVB was one of the banks that lobbied Congress and the Trump administration for this exemption. Originally all banks with more than $50B in assets would be required to submit to stress tests, but after the new legislation was passed in 2017, this was raised to $250B. This deserves another look to raise the profile of excessive risk at banks before a bank run happens.

How will this affect the tech labor market?

Another area that hasn’t received much coverage is how this will affect the tech labor market. VCs and LPs were already spooked by the bank run at a time when funding was already declining. That would mean less hiring and potentially more layoffs if business was interrupted over the weekend. We’ll still have to wait for the dust to settle to see if this will cause closures at some small startups or if loans and VC support are enough to prop up the smallest (or most cash-strapped) players.

More resources

Why was there a run on Silicon Valley Bank?

The death of Silicon Valley Bank

Startup bank had a startup bank run

Have comments, questions, or clarifications? Please leave it in the comments section below!